Central Valley Multifamily Market Update – Q1 2026: Cap Rates, Demand & Investment Outlook

Central Valley Multifamily Market Update – Q1 2026

The Central Valley multifamily market continues to evolve in a higher interest rate environment, with rising cap rates, resilient investor demand, and improving transaction activity shaping the landscape in early 2026.

Multifamily Cap Rate Trends in the Central Valley

Multifamily cap rates have increased from peak 2022 pricing, but remain competitive relative to long-term historical averages.

2025 Average Cap Rate: 6.15%

2022 Peak Pricing: 4.96%

20-Year Average (Since 2004): 6.71%

While cap rates have expanded in response to higher interest rates, pricing levels indicate that investor demand for Central Valley multifamily assets remains strong relative to historical norms.

Transaction Volume & Investor Activity

Multifamily transaction activity rebounded in 2025, signaling renewed market momentum.

Total Transactions (2025): 79

Increase vs. 2023: +27%

Prior Peak Average (2017–2022): ~122 annually

A notable shift has been the increase in local buyer activity, with 49% of purchasers based in the Central Valley, reflecting growing confidence from in-market investors.

Central Valley Rent Growth Outlook

Rent growth has remained muted over the past 18 months due to elevated supply and affordability constraints.

Recent Rent Growth: ~1.3% year-over-year

Projected Growth: 2–3% annually

As new supply is absorbed and demographic trends remain favorable, rent growth is expected to normalize to sustainable levels.

Economic Drivers Supporting Multifamily Demand

Several key economic factors continue to reinforce the region’s multifamily fundamentals:

Healthcare Expansion: Approximately 14,500 healthcare jobs projected in Fresno County between 2023 and 2028, supporting workforce and market-rate housing demand.

Entertainment & Hospitality Growth: New developments, including the Hard Rock Casino in Kern County and additional projects in Madera, are expected to generate employment and regional economic activity.

Industrial & Logistics Development: Facilities such as Gimme Health Foods and AutoZone in Madera are contributing an estimated 500+ jobs.

Long-Term Industrial Pipeline: Continued investment in industrial infrastructure is expected to drive sustained job creation and housing demand across the Central Valley.

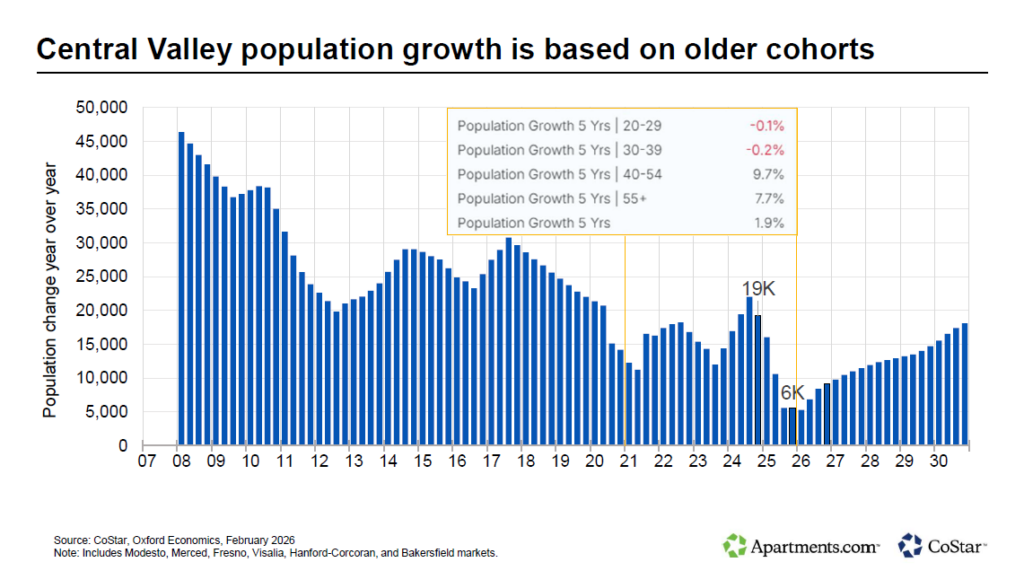

Population Trends & Long-Term Outlook

Population growth in the Central Valley continues to trend positive, with notable strength among older demographic cohorts. This supports long-term housing demand across multiple renter segments and reinforces the stability of the region’s multifamily market.

Multifamily Investment Outlook for 2026

Despite higher interest rates, multifamily investment activity remains healthy, and investor demand persists for well-positioned opportunities.

As the regional economy expands and population growth continues, the Central Valley remains well-positioned for long-term stability and growth. Multifamily assets continue to attract investors seeking durable cash flow and exposure to a fundamentally undersupplied housing market.

Want to understand how these trends impact your property or investment strategy?